Insurance premium reconciliation: the complete guide

Key Takeaways

- Insurance premium reconciliation is fundamentally different from generic payment matching — one bulk broker payment can cover hundreds of policies, each needing individual line-level matching.

- The naming problem is worse than it looks. Brokers use abbreviated names, reordered names, trading names, or no insured name at all — and exact string matching catches almost none of it.

- Policy references are not standardised. Formats drift between brokers and sometimes between months for the same broker. Payments arrive against last year’s renewal reference.

- Closing advices are unique to insurance and the most overlooked stage of the cycle. Processing them on arrival prevents the majority of suspense items before any cash moves.

- Premium trust accounts change the risk profile. Unallocated cash isn’t just operationally painful — it’s a compliance concern.

- Format chaos is permanent. Any process that needs a template per broker will be in constant maintenance mode.

- The metric that matters is straight-through processing rate: 97%+ is achievable from day one, 99%+ with closing advice processing.

- The real cost isn’t hours — it’s staff dependency. When broker quirks live in one person’s head and that person goes on leave, the backlog grows.

If airlines ran baggage claim the way insurance brokers run remittance advices, many of the bags would have no tag, others would have the wrong tag, and most would contain clothing from several different passengers.

That’s insurance premium reconciliation. The “bag” is a broker payment. The “clothing” is a line on the remittance. The “passenger” is a policy. You can’t just match bag to name — you have to open each one, lay the contents on the floor, and work out whose shirt is whose.

I’ve spent six years working with insurance finance teams on this problem, and the thing that strikes me every time is how many reasons there are for things not to line up. The payment amount is wrong. The name is spelled differently. The policy reference is the broker’s internal code, not yours. The remittance is a PDF where someone has manually typed numbers into a table. One payment covers 83 policies from different policy holders, so you need to split it and match each line individually. The broker pays a single amount for a risk you have covered under two policies. The broker pays multiple amounts for a risk you have in your system as a single amount due.

A baggage handler facing this would quit. A finance team can’t.

This guide walks through every stage — what makes insurance reconciliation different from generic AR, what the data actually looks like when it arrives, how teams handle it today, what good automation looks like, and how to evaluate a solution without getting sold a template-based system in AI clothing.

What makes insurance reconciliation different

If you’ve come here from a generic “payment reconciliation” search, let me save you some time: the tools built for SaaS billing or B2B invoicing don’t work for insurance. They assume one payment matches one invoice. Insurance doesn’t work like that.

The multi-policy problem

A single broker remittance might cover 5 policies or 500. One payment that needs to be split and matched line by line. Each line has its own amount, its own policy reference, its own insured name. Every generic reconciliation tool I’ve evaluated falls over at this step. They can match one-to-one. They can’t split a single bank transaction across hundreds of individual policy lines.

It also runs the other way. One broker might send a $3.1M bulk payment covering one advice. Another sends four separate payments that together cover one advice. A third splits one monthly advice across three weekly payments. And sometimes a single line on the remittance maps to three different debtor records in your system that need to be aggregated to come close to the total paid — same insured, different policy records, one payment. Reconciliation has to handle all of these without flattening them into one-to-one matching that loses line-level detail.

The naming problem

This is worse than most people realise until they see it in production data. Here’s what actually happens when brokers list insured names on remittances — these are real patterns from our system:

Truncation. The remittance says “Zorvax Courier Servic” — cut off mid-word. The invoice says “Zorvax Courier Services Pty Ltd.” A human reads past this instantly. A string-matching algorithm sees two completely different names.

Abbreviation. The remittance says “OC XZ9021.” The invoice says “Owners Corporation XZ9021.” Same thing, different convention.

Reordering. The remittance says “Jaska Vexnira.” The invoice says “Vexnira, Jaska.” First-last versus last-first.

Person vs. business. The remittance says “C Drellix.” The invoice says “Chris Drellix T/as Phramis Productions.” The broker sent the insured’s personal name. The policy is under the trading name.

Partial entity names. The remittance says “VK Phramis.” The invoice says “V & K Phramis Holdings Pty Ltd.” Missing the entity suffix, dropped ampersand, no entity name.

Complete mismatch. The remittance says “Darlan Noxridge & Noxridge Pty Ltd.” The invoice says “Noxridge Pty Ltd and Darlan Noxridge.” Same parties, reversed order, “and” instead of ”&.”

No name at all. Sometimes the remittance just has a broker internal code where the insured name should be. The invoice has the full name. Good luck with your string matching.

A human figures these out because they know the broker. A matching algorithm that relies on exact or even partial string matching doesn’t stand a chance. You need AI matching that understands abbreviations, entity suffixes, name reordering, and trading name variations.

The policy reference problem

You might think policy numbers would be standardised. They’re not.

A broker sends “03PRPI0038137R” on their remittance. Your invoice system has it as “03-PRP-I-0038137.” Same number, different formatting — hyphens stripped, segment boundaries ignored, and an “R” suffix the broker has tacked on to indicate a renewal. Or the remittance shows “MARSTR20323812” and the invoice has “MAR-STR-20323812.” Or the broker sends a completely different reference system — their internal code, a composite of multiple fields mashed together, or occasionally just “T/B/A.”

Policy year differences are common. The remittance references “CYB-015262-2024” — last year’s policy. The invoice is “CYB-015262-2025” — the renewal. It’s the same policy, rolled over. The broker is paying against the old reference because that’s what’s in their system.

Endorsements add another layer. A broker remits against a policy number without specifying which endorsement. You have an original policy and three adjustments on the books, and the payment could apply to any combination of them. You have to work out which.

Short-pays, overpayments, and adjustments

Brokers frequently remit less than the full premium. Sometimes it’s a legitimate commission correction. Sometimes a mid-term cancellation. Sometimes they’ve applied a credit from a different policy. Sometimes it’s just wrong. Each short-pay needs a decision: accept the adjustment, or query the broker. And you need to make that decision across dozens of lines on a single remittance.

Overpayments are rarer and arguably worse. The broker sends too much. Now you’re holding money that doesn’t belong to you in a trust account, and working out who it belongs to requires the same detective work as a short-pay — plus the audit trail saying the cash is not yours.

Closing advices

Before payment arrives, brokers send closing advices — documents confirming the terms and amounts for premiums they intend to remit. Closing advices are unique to insurance. Most AR tools don’t know they exist, let alone process them.

When you match closing advices to invoices on arrival, discrepancies surface 30-60 days before payment. Without them, you only discover problems when the payment doesn’t match — and by then the broker has moved on. (Full argument here: why closing advice processing is the highest-leverage change most finance teams aren’t making.)

Format chaos

There is no standard format for a remittance advice. PDFs, CSVs, Excel files, plain-text emails. Even within the same broker, the format changes between months. One broker we onboarded had sent three different CSV layouts in the same quarter. Any reconciliation process that needs a template per broker is going to be in constant maintenance mode.

Here’s what “no standard format” actually looks like. These are six real remittance PDFs from our production system, de-identified (broker and underwriter letterheads blurred, insured names and policy numbers replaced with fakes, amounts preserved). Each is from a different broker or payer. Each covers a different book of business. Each lands in a finance inbox on the same morning, sometimes dozens at a time.

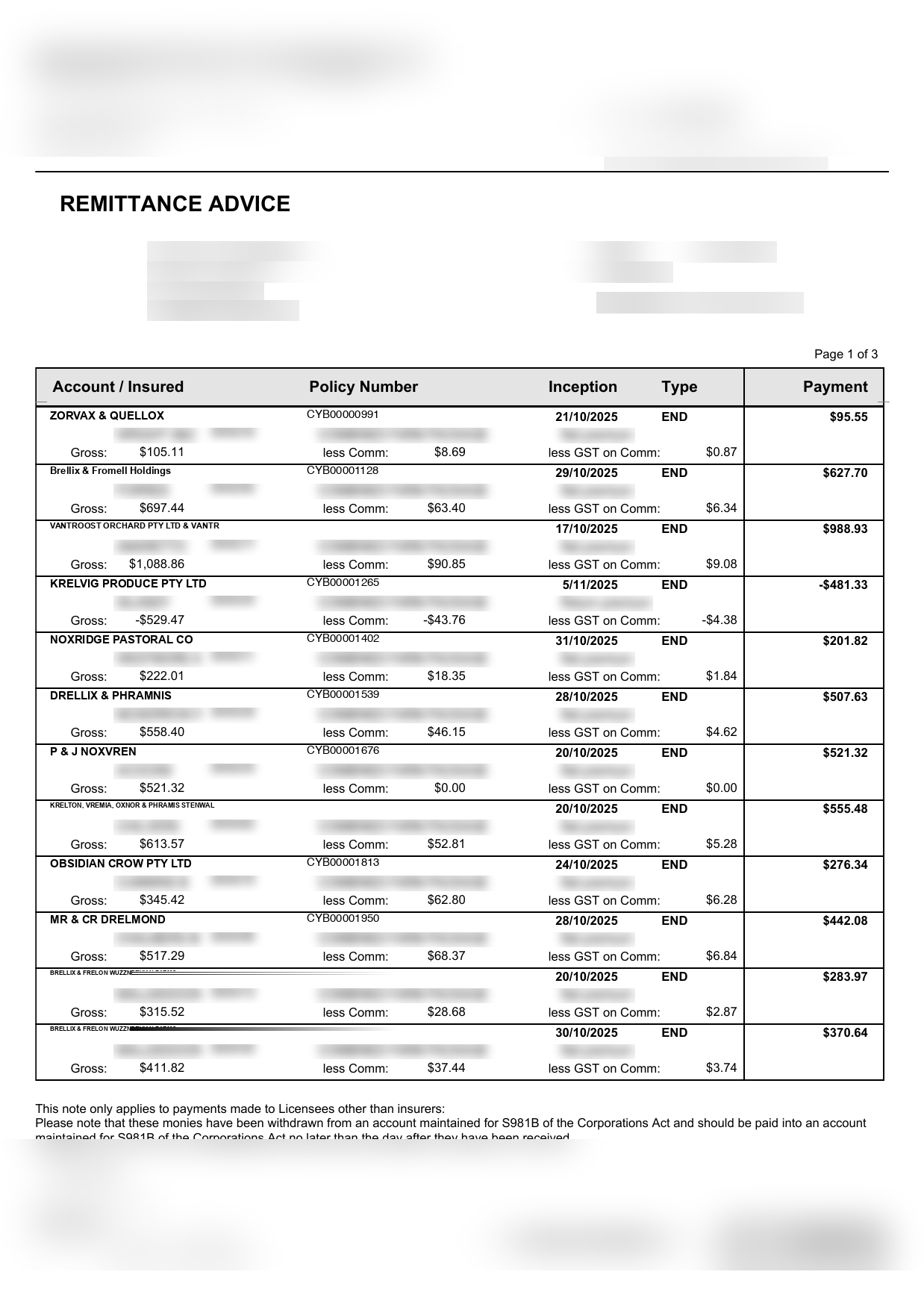

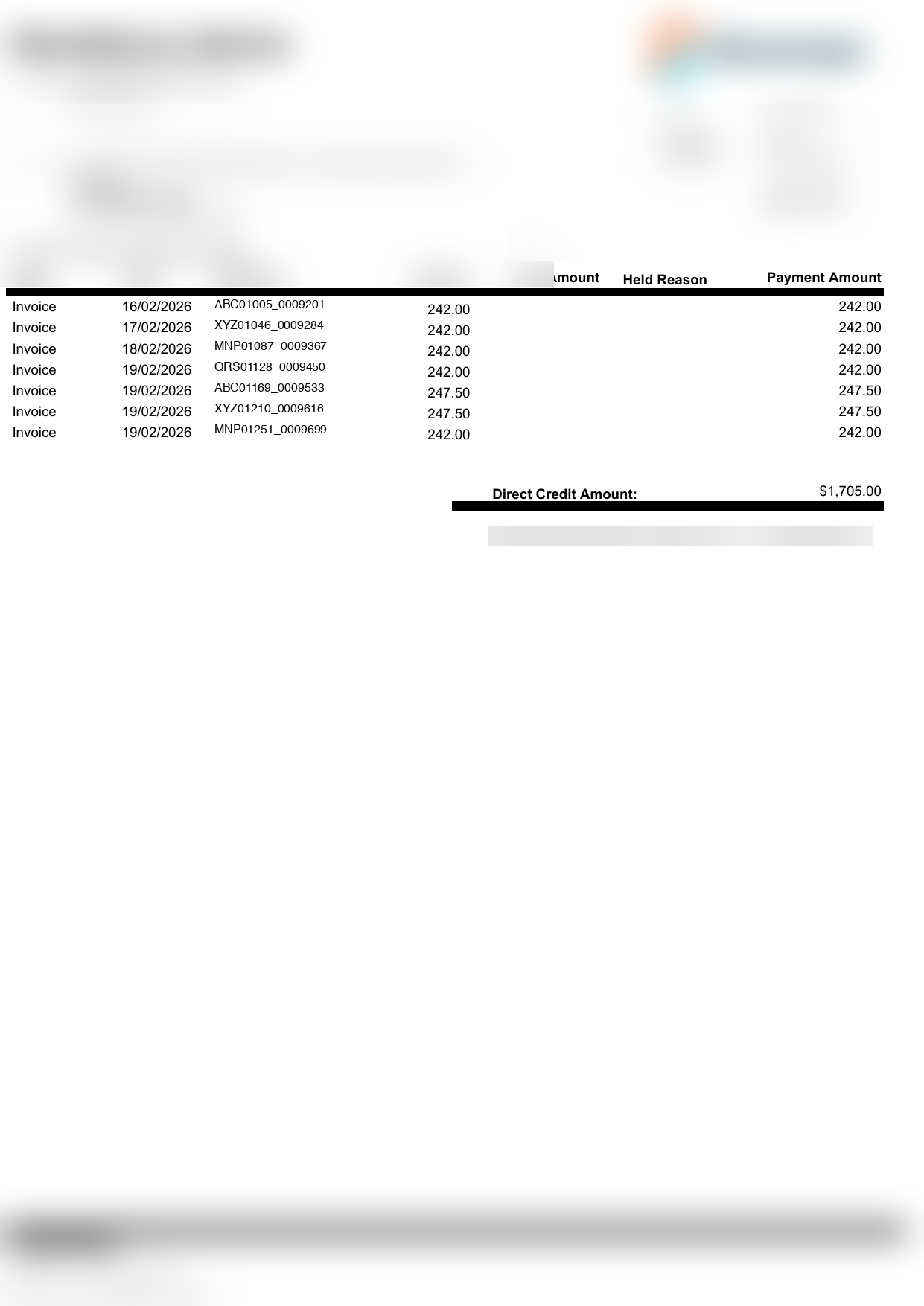

A multi-section farm-package remittance. Thirty-one policies across a single payment. Each line has an insured name, a policy reference, a combined-package section header, and a three-line breakdown of gross / commission / GST. Two lines are negative (reversals from prior endorsements).

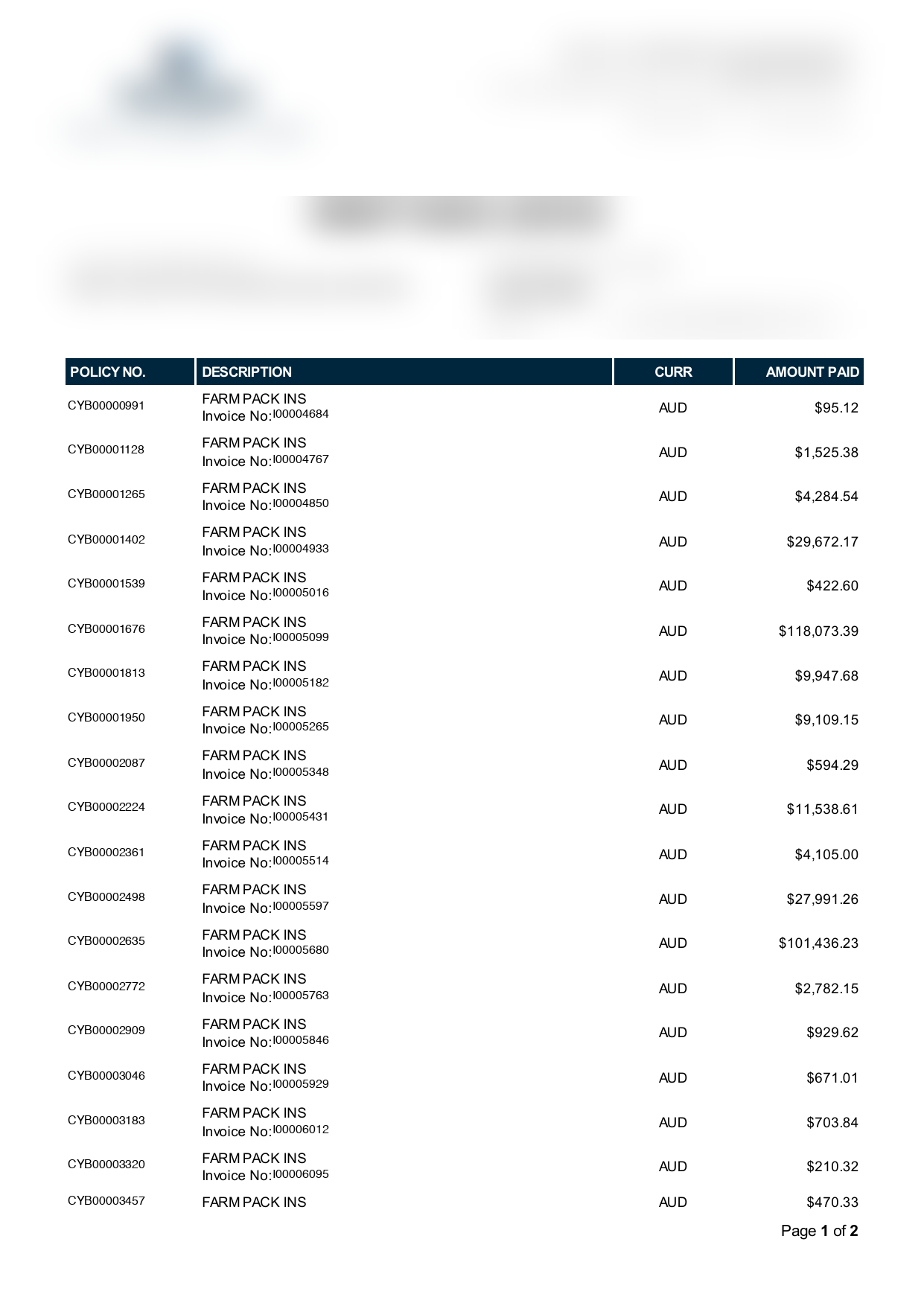

A flat list from a large national broker. Twenty-four policies, all tagged “FARM PACK INS”, each with a policy number and an internal invoice reference. Pagination continues over multiple pages. No insured names on the remittance at all — the underwriter has to match on policy reference alone.

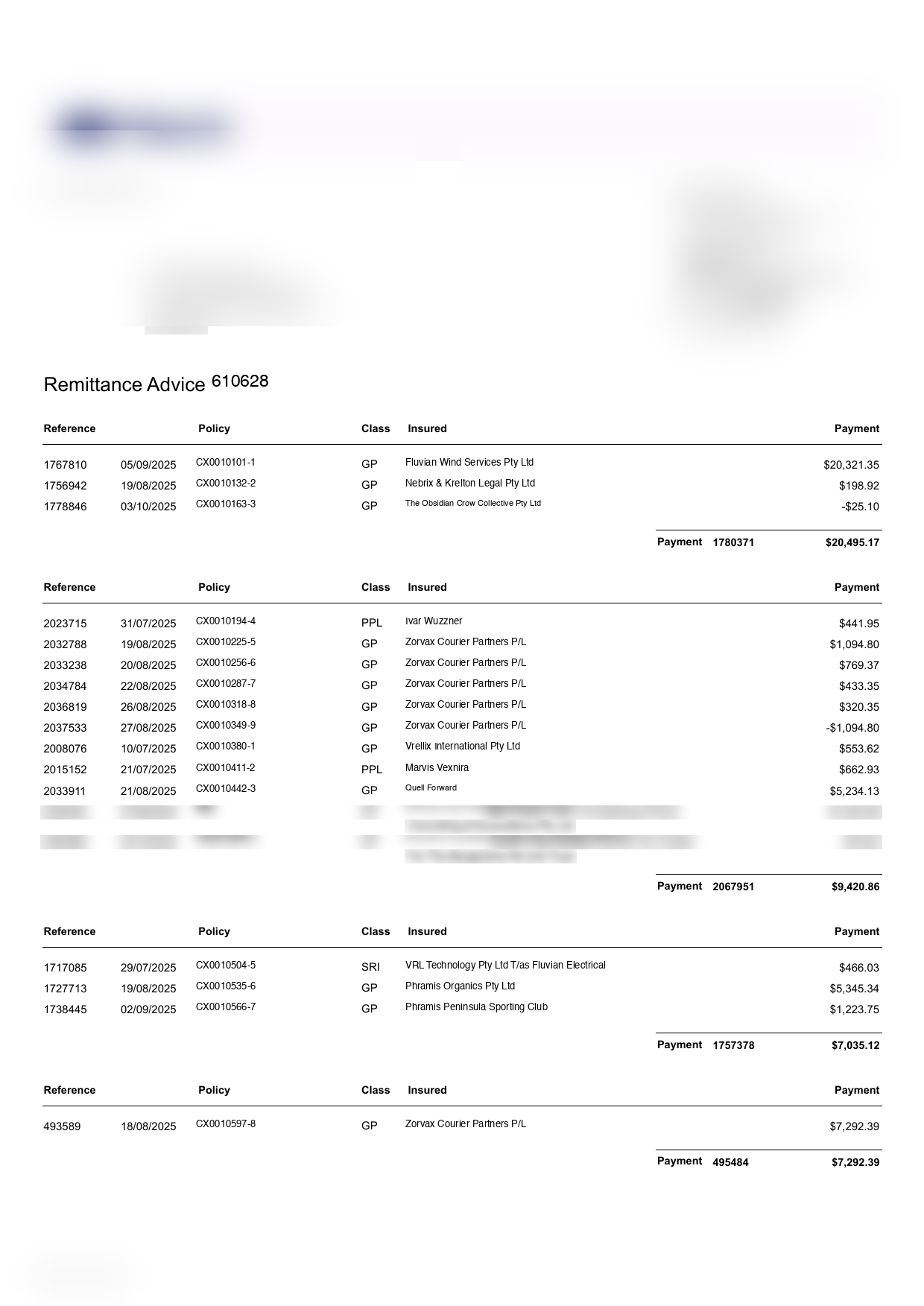

A remittance from a global broker. Twenty-three policies across multiple classes (General Property, Public Liability, etc.). Policy references use a hyphenated multi-part scheme, insureds include a mix of trading names, sole traders, and trusts. One insured appears four times in a single advice across different policies.

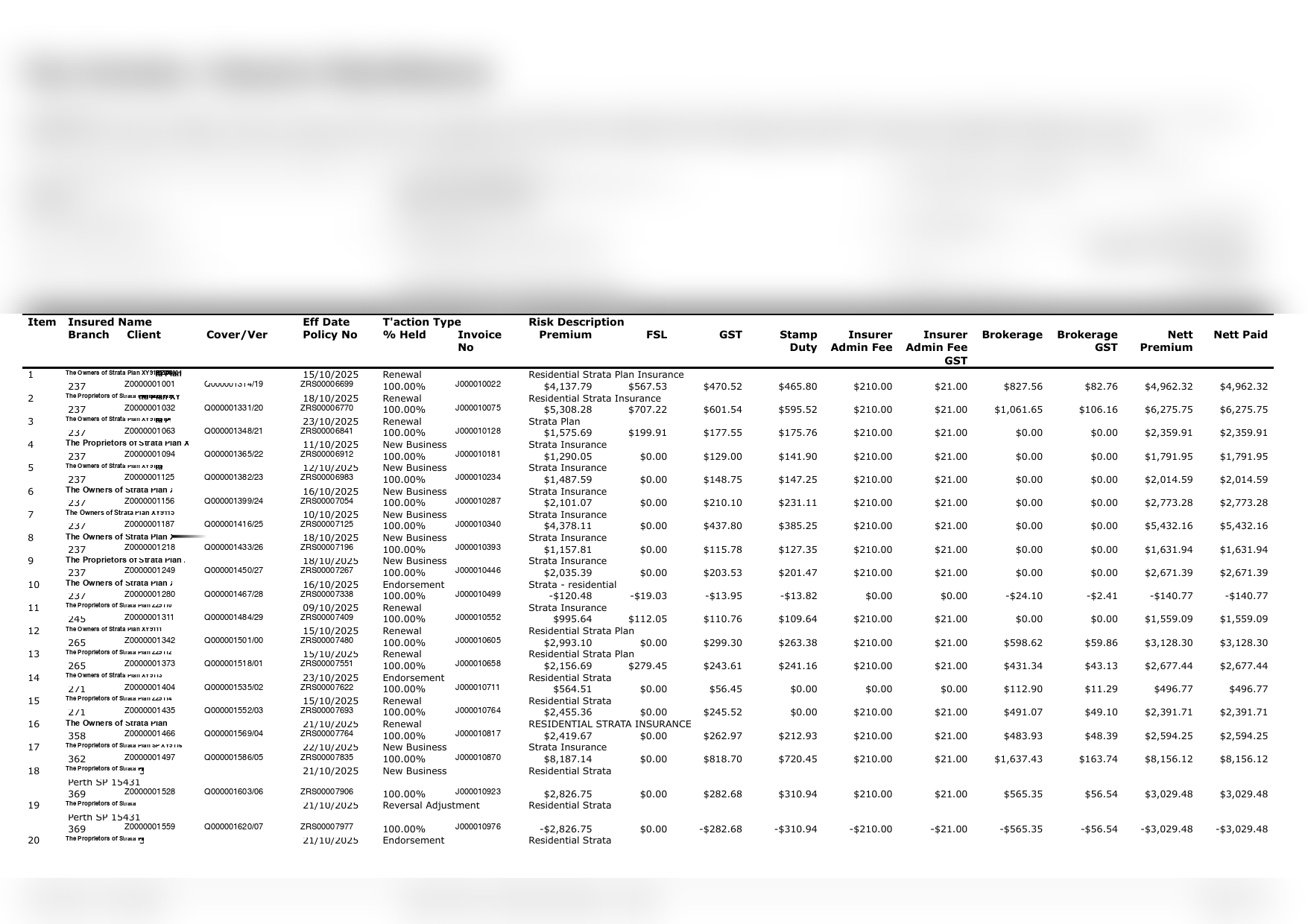

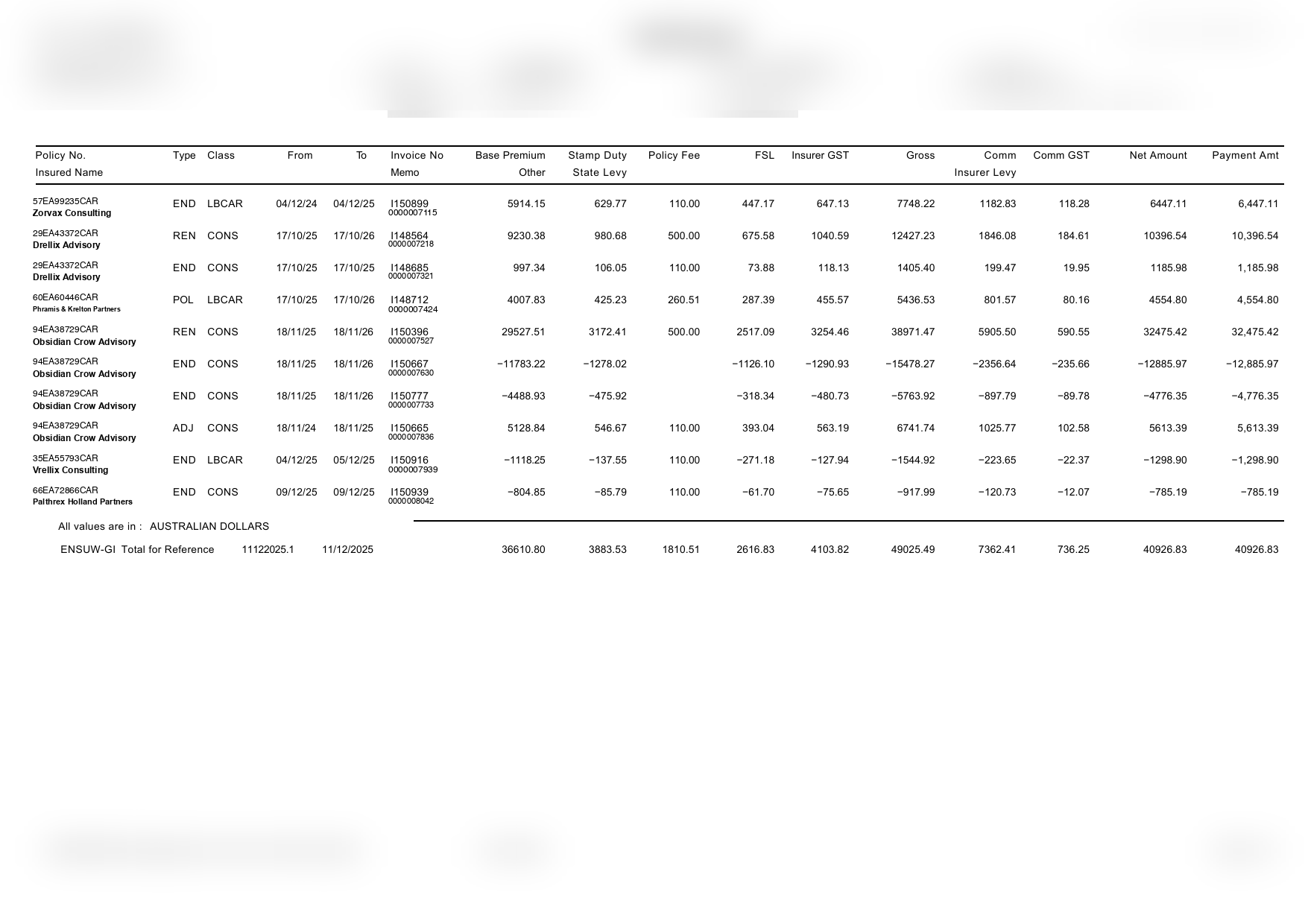

A “Tax Invoice –Insurer Remittance” from a cluster group broker. Fifteen financial columns per row — policy number, effective date, transaction type, percent held, invoice number, risk description, premium, FSL, GST, stamp duty, insurer admin fee, brokerage, brokerage GST, net premium, nett paid. Twenty-seven lines on the page. Each cell is a small number in a narrow column. Staff running this through manually get headaches.

A specialty broker’s “Remittance Advice” — ten policies across a single advice. Sixteen columns ranging from policy number, transaction type, class, from/to dates, invoice number, base premium, stamp duty, policy fee, FSL, insurer GST, gross, commission, commission GST, net amount, to payment amount. Column abbreviations vary by broker: what one calls “Net Amount”, another calls “Nett Paid”, another calls “Payment Due”.

Not every remittance comes from a broker. This one is from a commercial insured paying directly — a transport operator covering CTP-style claims management fees. The “reference” is the broker’s internal claim number, the “payment amount” repeats identically, and the insured name doesn’t appear on the advice at all. Matching this to anything requires an external reference lookup.

Now imagine a finance team opening forty of these every morning, each in a different format, and trying to line up each line with an outstanding premium in their policy admin system. That’s the problem before any of the name mismatches, policy reference drift, or short-pays come into play.

Premium trust accounts change the risk profile

Broker premiums sit in a trust account — regulated under APRA, the FCA, or equivalent, depending on jurisdiction. That has two consequences generic AR tools miss.

First, cash can’t sit unallocated indefinitely. The money in the trust account isn’t yours until it’s matched to a policy. Suspense items aren’t just operational annoyance — they’re a regulatory exposure. Cash held unallocated for weeks starts to look like a trust account control failure.

Second, misposting is worse than not posting. Allocating the wrong amount to the wrong policy can trigger chargebacks, commission reversals, and regulator attention. The pressure to “just resolve it” has to be balanced against the cost of getting it wrong. Manual matching errors don’t just cost time to fix — they have a compliance tail.

Any tool that pretends insurance AR is the same as generic invoice matching misses both of these.

How most teams do it today

Without automation, insurance premium reconciliation goes like this every morning:

- Download the bank statement and identify broker payments

- Find each remittance attachment in the broker’s email — open the PDF or CSV or Excel

- For each line on the remittance, search your policy admin system for a matching outstanding premium

- Handle the name mismatches, the wrong policy references, the short-pays

- Key the matched amounts into Xero, UPM+, Entsia, or whatever your back-office system is

- Move unmatched lines into a suspense spreadsheet

- Email brokers about short-pays and missing references

- Come back tomorrow and do it again

For a team processing payments from 50+ brokers, step 3 alone — the searching and matching — runs to 30+ hours per month. And the error rate on manual keying adds its own risk. I’ve seen misposted allocations that took weeks to surface because nobody caught the transposition.

Step 7 deserves its own callout. In a manual process, broker queries are emails from personal inboxes, threaded with whatever subject line the broker chose, with no audit trail back to the specific unresolved line. When the broker replies two weeks later — “re: re: re: your query” — the person who sent the query has moved on to other things and the context takes ten minutes to reconstruct. That’s before anyone thinks about the compliance auditor asking to see correspondence for a specific suspense line from six months ago.

What automated reconciliation looks like

Automated insurance premium reconciliation replaces most of those steps. Remittance advices in any format get read and structured automatically — no templates, no manual data entry. Each line is matched to one or more outstanding premiums using policy references, insured names, amounts, dates, and broker context. AI matching handles the naming chaos. Amount tolerances handle rounding.

Lines that can’t be matched go into a managed queue — not a spreadsheet — with context about what was tried and why it didn’t match. Discrepancies trigger structured queries to brokers with replies tracked against the correct suspense line. Matched allocations get posted directly to the policy admin system without anyone touching a keyboard.

The number that matters is straight-through processing rate: what percentage of remittance lines get matched and posted without a human touching them. A well-built system achieves 97%+ from day one, and 99%+ when closing advice processing is running alongside it. (The DSO piece explains how the pieces compound — and why each stage on its own only moves the needle so far.)

The posting step — where most automation dies

There’s a step people forget when they talk about “automation.” Matching is one thing. Getting the matched data into Xero, UPM+, Entsia, eGlobal, or whatever your policy admin system is — that’s another.

Plenty of tools solve the matching problem and then produce a CSV for someone to import. That’s not automation. That’s moving the manual step, not removing it.

Real automation pushes the allocation into the policy admin system directly — premium allocations, commission splits, tax components, all posted against the correct policy line. Short-pays get flagged for approval before posting, not after. Overpayments land in a suspense ledger with an audit trail. If the policy admin system rejects an allocation, the matching tool surfaces the rejection — not a silent error in a log file nobody reads.

If a tool hands you a report that “just needs importing” and calls that the finished product, assume it’s adding a step, not removing one.

In practice, the rollout we run most often is two-phase. On day one the system generates a file the finance team imports into the policy admin system — not because that’s the end state, but because it means they can start getting value the same day without waiting on IT. Then, when the IT team has time and capacity, we build the direct integration and the import step disappears. The matching is working from the start. The plumbing catches up when the calendar allows.

Approaches to automation

There are several ways to approach this, each with trade-offs.

Template-based extraction

The oldest approach. You configure a template for each broker’s remittance format — map column A to policy number, column B to insured name, etc. It works until the broker changes their spreadsheet layout, which they will. If you have 50 brokers, you’re maintaining 50+ templates. Some teams employ dedicated staff just for template maintenance.

RPA (Robotic Process Automation)

RPA bots can be scripted to open emails, download attachments, navigate your policy admin system, and key in matches. The problem is brittleness. Every UI change in your admin system breaks the bot. Every new broker format needs a new script. And RPA can automate the keying but can’t solve the matching — it still needs a human to decide which invoice matches when the reference doesn’t match exactly.

Bespoke AI models

Train a model on your broker remittances. Retrain when formats drift. Gather samples, label them, run through a training pipeline, ship the new model. It works, but it’s a treadmill. Every new broker means a fresh training cycle. Every new country or region means a fresh dataset. This is what we did for years before general-purpose AI made it obsolete.

General-purpose AI matching

This is where the industry is moving. An AI that reads any remittance format without templates, understands names and references with the flexibility of a human reader, and posts allocations into the back-office system. No configuration per broker, no maintenance when formats change, no retraining when a new market appears.

The advantage over template-based systems is obvious: no configuration per broker, no maintenance when formats change. The advantage over RPA is that AI can actually solve the matching problem, not just automate the keying around it. The advantage over bespoke models is that one system works everywhere — new broker, new country, new language, same engine.

How to evaluate a solution

If you’re looking at automation options, here’s what separates tools that work from tools that demo well:

Multi-format ingestion without templates. Drop any file the broker sends in — PDF, CSV, Excel, email body, scanned image — and see if it reads. If the vendor needs a week to “configure the template,” you’ll be configuring forever.

AI matching on real data. Bring your messiest remittance to the demo. The one where the broker abbreviated the insured name, reversed the policy reference, and short-paid by $8.40. If the tool matches it live, it’s real. If it needs “a short training period,” it’s template-based dressed up in AI language.

Closing advice processing. A tool that only acts at payment time is missing the most valuable stage. This is the single biggest differentiator between AR tools built for insurance and AR tools built for everything else.

Direct posting into your policy admin system. Not a CSV export. Not a “report.” Actual allocations, actual commission splits, actual line-level posting into Xero, UPM+, Entsia, or whatever you run.

Suspense queue with structured communication. When a line doesn’t match, you need a managed queue with broker queries tied to the line, replies routed back automatically, and an audit trail a regulator could follow. Not an email inbox. Not a spreadsheet.

Premium trust awareness. The tool should understand that unallocated cash in a trust account has a compliance dimension, not just an operational one.

Straight-through processing rate transparent on day one. If a vendor won’t show you their STP rate on a random sample of your actual data, the number doesn’t exist. Good vendors will sit with you and match a live batch.

What to measure

If you’re running insurance AR today — automated or not — these are the numbers to watch:

- Straight-through processing rate. Share of remittance lines matched and posted without human intervention. 97%+ is achievable. Below 80% means the tool isn’t doing the work.

- Average age of suspense items. How long unresolved lines sit before they’re cleared. Anything above two weeks is a signal that broker queries aren’t being tracked properly.

- Suspense inflow vs outflow. If more items come in each week than get resolved, the pile grows regardless of how good the matching is.

- Days from cash receipt to cash allocation. The portion of DSO entirely within your control. Best-in-class is same-day. Typical is 7-10 days. Worst is “it depends on how busy we are this week.”

- Manual touches per remittance. Number of human interventions per payment processed. The goal is zero for matched lines, one for exceptions.

None of these come out of the box from the policy admin system. You either build them from matching logs or use a tool that surfaces them by default.

The staff dependency problem

Beyond the hours, there’s a risk that doesn’t show up in time-tracking: institutional knowledge. Knowledge of broker quirks — which ones use weird references, which ones always short-pay, which ones send closing advices that don’t match their remittances — lives in one person’s head.

When that person goes on leave, the backlog grows. When they leave the company, it’s worse. I’ve seen finance teams lose months of progress when their most experienced reconciliation person moved on, because nobody else knew the broker patterns well enough to match efficiently.

Automation captures that knowledge in the system rather than in someone’s head. The matching engine learns the broker patterns once and applies them consistently, regardless of who’s sitting in the chair. The best tools also make the knowledge visible — you can ask them why a line matched the way it did and get a straight answer.

Getting started

If you’re matching broker payments manually, the first step is quantifying the problem: how many hours per week, how many suspense items, how long they sit before resolution, how many different remittance formats you receive in a typical month. That’s your baseline, and it’s usually worse than people think.

From there, the decision is straightforward. Template-based tools will put you on the treadmill. RPA will automate the keying without solving the matching. Bespoke models will work until the next region or the next broker. General-purpose AI is the only approach that handles the full mess without adding its own maintenance burden.

If your team is in this situation, I’d like to show you what we built. Book a demo — bring your messiest remittance and we’ll match it live.